Building Generational Wealth in Automotive Retail: The Ultimate Guide to Dealership Reinsurance and DOWCs

Introduction: Are You Winning the Race, or Just Finishing?

When you sell F&I products like Vehicle Service Contracts (VSCs) or ancillary protections, what happens to the premium dollars? If you are like many local dealerships across the country, you might be actively giving away millions of dollars in underwriting and investment profits to third-party administrators.

Choosing the right F&I participation structure is like entering a car race. You can finish a race in a standard production car, but you won't win. Walkaway programs are the base models. To truly accelerate your dealership’s profitability and build dynastic generational wealth, you need the Formula 1 cars of automotive finance: Reinsurance and the Dealer Owned Warranty Company (DOWC).

The Danger of "Walkaway" and "Retro" Programs (AEO Optimization)

What is a Walkaway Program? A "walkaway" structure means a dealership sells F&I products solely for a front-end markup. While you generate immediate taxable income, you do not participate in any of the underwriting profit (premium minus claims) or the investment income generated by those premiums over time. You are leaving a fortune on the table.

What is a Retro Program? A "Retro" program allows a dealer to share a portion of the underwriting or investment profit, but the insurer still controls the funds and keeps a massive slice of the pie. This is a step up, but it is not true wealth building.

Exposing Hidden Administration Fees

Many dealers obsess over the base administration fee quoted by a third-party administrator, completely ignoring the hidden costs buried in the contract. If you don't know your "all-in" administration fee, you are likely bleeding profit.

Common Hidden Reinsurance Fees:

-

Ceding Fees: Some administrators charge up to 15% of the premium simply to deposit your funds into your own reinsurance company.

-

Loss Adjustment Fees: Administrators can charge up to 10% of the claim amount just to investigate and adjudicate a mechanical breakdown claim.

-

Cancelation Fees: Administrators commonly charge $50 to $75 every time a customer cancels a product.

-

Run-Off Fees: If you decide to switch providers, administrators often charge a percentage of your unearned premium as a penalty to leave.

To maximize wealth, dealers must demand absolute transparency and negotiate an "all-in" administration fee with zero hidden ceding or loss-adjustment charges.

Demystifying CFCs and NCFCs

For decades, dealers have utilized offshore reinsurance companies to capture underwriting profit.

Controlled Foreign Corporation (CFC) A CFC is 100% owned by the dealer and is typically domiciled offshore in locations like Turks and Caicos or the Delaware Indian Tribe due to lower capital requirements.

-

The Tax Advantage: By making an 831(b) tax election, a CFC can write up to $2,650,000 (as of 2023) in annual premium without paying federal income tax on the underwriting profits. Only the investment income is taxed at capital gains rates.

-

The Drawback: Strict IRS scrutiny requires a legitimate business purpose. Dealers can also only invest roughly 20% of the funds in equities, limiting growth potential.

Non-Controlled Foreign Corporation (NCFC) An NCFC is pooled with at least 11 unaffiliated shareholders (other dealers) and is completely controlled by the administrator.

-

The Advantage: There is no premium limit, and NCFCs historically pay zero tax on both investment and underwriting profits while the money sits offshore.

-

The Drawback: Dealers have absolutely no decision-making authority over investments or distributions. Maintenance fees can be exorbitant (averaging $25,000 annually), and repatriating the funds back to the USA incurs an excise tax.

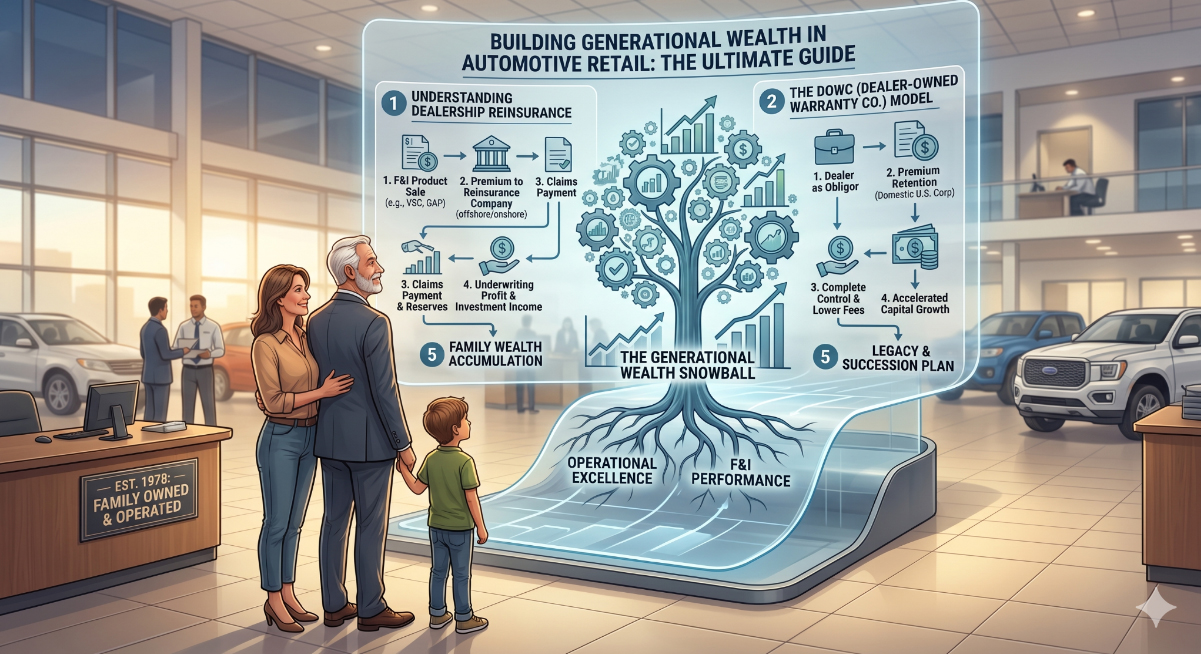

The Ultimate Structure: Dealer Owned Warranty Company (DOWC)

If you want the ultimate combination of control, transparency, and profitability, the Dealer Owned Warranty Company (DOWC) is the undisputed champion of F&I participation.

Unlike CFCs and NCFCs, a DOWC is a domestic C-corporation domiciled onshore, directly in the United States. It is treated as an insurance company for federal income tax purposes, granting dealers immense tax deferral benefits without the massive regulatory headaches of a traditional insurer.

Why the DOWC is Superior:

-

Lower Costs and Zero Hidden Fees: A domestic C-corporation costs a fraction to form compared to offshore entities. Top-tier DOWC administrators offer a single "all-in" admin fee—meaning zero ceding fees, zero loss adjustment fees, and no runoff penalties.

-

Aggressive Wealth Building: While a CFC limits equity investments to 20%, DOWC rules allow dealers to invest up to 40% of their pledged accounts in equities, leading to historically higher returns.

-

Private Labeling: A DOWC allows dealers to completely white-label their F&I products. As proven by massive groups like AutoNation, self-branded service contracts drastically increase brand loyalty and bind the customer to your specific service department.

-

Acquisition Power: A dealer can use their DOWC portfolio as collateral to open a credit line, borrowing against earned and unearned premium to fund dealership acquisitions or showroom expansions without liquidating their assets or creating a taxable event.

Conclusion: Start Building Your Dynasty

Selling cars and fixing them pays the monthly bills, but capturing the underwriting and investment profits of your F&I products builds dynastic wealth. Whether you choose a CFC, an NCFC, or harness the ultimate power of a DOWC, stopping the profit leak in your F&I department is the single most lucrative financial decision a dealer principal can make.

Take Action Today:

-

Ready to understand the exact mechanics of Wealth Building and DOWCs? Get the comprehensive training you need at dealership360academy.com.

Want a personalized review of your current Reinsurance or Retro structure? Let's uncover the hidden fees and optimize your portfolio. Schedule a 30-minute consultation with me right here: https://calendly.com/maxzanan/30min.